Pricing Agriculture Risk | Interview with Grant Cavanaugh

Commodities, onion derivatives, and catastrophe modeling with the CIO of Scoot Science

This is Part Two of a Two-Part food and commodity inflation series. I wanted to intro Scoot on Wednesday as a solution, and this is a follow up broader macro piece.

If you’re already subscribed, thank you! If you’d like to subscribe, please do so here:

YouTube up later today, podcast up now!

I got the chance to interview Grant Cavanaugh, the CIO of Scoot Science, a PhD in Agricultural Economics and is just generally quite brilliant - he has spent time in reinsurance, derivatives, and more. We talked about pricing risk - what does agricultural risk *really* mean - and dove into the more nuanced mechanics of the weirder parts of the commodity markets (including onion derivatives!)

The full interview is below - (edited for clarity, and emphasis on select parts for takeaways)

Some Brief Kyla Thoughts Before

The below flowchart is how the world has (sort of) worked around globalization and trade. We have relied on a global world that functions just-in-time for the better part of the last century - but things like war and pandemics begin to break the functionality. It’s obviously really simplified, but there are some things that I want to highlight.

How a Global World Normally Works: Globalization is a core component of our system. A lot of countries rely on imports for the majority of their consumption - and that’s not a BAD thing. It’s really good! That means that countries that are better at producing some sorts of goods can produce them (comparative advantages) - the utilization of resources is more effective across the board.

Impacts to the Global World: However, as we have seen from both the pandemic and the war in Ukraine, globalization can get disrupted. All of the sudden, the wheat exports, fertilizer, oils, etc from Russia and Ukraine are uncertain - which reverberates down the entire supply chain.

Countries like Egypt that import billions of dollars of wheat from Russia and Ukraine both are suddenly left without many options - and globalization is no longer a solution, but a problem.

Compound that with supply chain issues, floods, and fires, and food sources are no longer as stable as they once were (or as we *expected* them to be).

Normal Trade Process: And everything is an input-output process too - so natural gas goes into fertilizer, fertilizer goes into crops, etc. So if one domino tips, the entire line begins to topple. Russia is a huge exporter of natural gas, Belarus is a huge exporter of potash, a key part of fertilizer (which has already increased 3-4x in cost) and the loss of that impacts food production.

So then you get into the impacted trade process and the results

Domestic Protectionism: Countries are going to start to produce more goods domestically and try to wean off imports in general. This could lead to less exports, as countries stockpile goods for their people. Essentially, the globalization framework unravels and countries exist in silos (to build out the stock of their *silos*).

Shortages Lead to Broader Problems: This is something that many analysts have brought up - the echoes of political instability, like what happened with Arab Spring, due to lack of food.

Odd Lots had a good episode on this, with a few points

Countries should (1) not hoard their supply and (2) try to increase aid by supporting agriculture in developing nations

In the US, only 15% of our food costs represent the cost of a raw commodity - but in places like Egypt its much more 1:1

Developing nations are going to be squished out by developed nations - we already see this happening with Pakistan and diesel, and it’s just going to be important to keep an eye on

Solutions: As The Lykeion wrote in their piece, “the advent of the Internet of Things, Artificial Intelligence, and Big Data should help even more, as farmers can program fertilizer and water to feed crops at specific times to reduce waste and boost yields. Gene editing should help yield disease and drought-resistant crops, and both vertical farms and synthetic meats offer unique new possibilities to increase production while decreasing waste.”

Humans are very smart. There will be solutions that arise, as Grant and I discuss in the main piece.

Here are some of my favorite quotes from our interview!

Even with really big, nasty problems, you can break it up into constituent parts and start wrapping your mind around it in a functional way.

I always loved the story of futures on opening weekend at the box office. The film industry lobbied to kill it. And then of course, onions where the government has collectively said we will not trade futures in these contracts, in perpetuity seemingly.

There's also all sorts of markets where there's a real gap between the actual commodity that is produced and the thing that's traded on the marketplace. To the extent that those gaps exist - they feel kind of theoretical in times of normalcy. But in times of crisis, when you really genuinely need this type of commodity in this type of place, that's when you see weird dislocations, like what's happened in nickel.

That diversity within a market always leaves a market vulnerable in times of acute stress.

Like there's no tomatoes futures contract because the quality of tomatoes varies too much. We can't even get close to a circumstance where we all are looking at the same page when it comes to the price of tomatoes.

I think it's the deviation from people's expectations that creates the real chaos in markets in the short term.

When you see really acute periods of nasty, food insecurity, famine type situation, it's often because the exchange rate between livestock and edible food goes wild.

In the short term, the salmon haul is going to be what it's going to be. That creates electricity type displacements in the marketplace than a lot of other commodities.

Even when you talked about this world where things normally feel scarce, you're referencing people's expectations and people's expectations are actually at this point, pretty darn efficient in the world of agriculture.

And it felt like there was a lot of pushback against the technological package in which those good intentions and success arrived.

Periodic commodity crises are opportunities at least to remember that that there's a lot happening in the world's communities. Even when we can go 10, 15, 20 years collectively not paying all that much attention.

Grant Cavanaugh

Catastrophe Research

Kyla: You have an *extensive* background in catastrophe research. Can you explain a bit of what you’ve done over the past couple of years?

Grant: I always knew that I wanted to work on agriculture. I went to a feeder school for the US State department and I got to see a lot of cool and interesting puzzles. I've worked on both the property and casualty side of insurance.

Property is hurricanes hitting the east coast of the United States, if you had to pick one single risk to sum it all up.

Casualty is more so the search for the next asbestos - the equivalent of a hurricane hitting Miami is asbestos in the world of casualty.

I've worked on both of those as a modeler - making statistical models of these risks and how they merge over time and what we should think about them.

Kyla: How do you measure and think about that risk? How do you price out something that theoretically no one knows is going to happen?

Grant: There's a lot that people don't know, but even with really big, nasty problems, you can break it up into constituent parts and start wrapping your mind around it in a functional way. For example, in 1992, Hurricane Andrew hit Southern Florida, the Bahamas and Louisiana. That was a really big event for reinsurers.

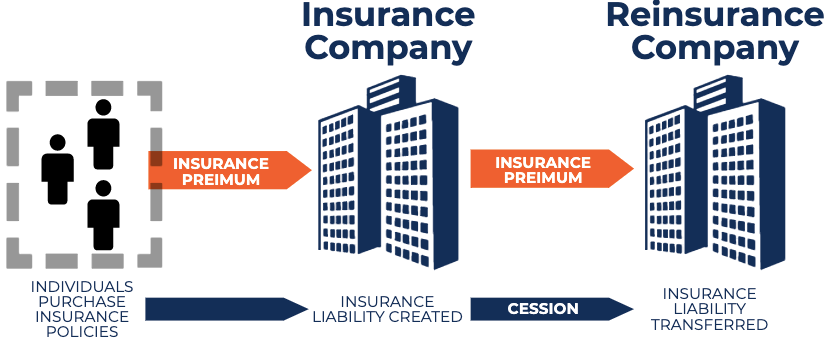

The insurance company itself is gathering up a lot of risk and ultimately trying to efficiently pass it on to a reinsurer, who's really in the business of saying, is there going to be catastrophic event or not?

So reinsurers are the ones who are really taking those big risks associated with hurricanes and earthquakes.

The only way that you could put money to work in these reinsurance markets was by just buying their equities. People started thinking, “what if we had alternatives and what kind of tools would support the alternatives?” and the tools that emerged were what are called catastrophe models.

So (1) hurricanes and (2) earthquakes are the big two property risks globally. How the modeling process works -

There's a couple of companies, RMS, CoreLogic, etc - that provide big models

They hire structural engineers to simulate buildings and building codes

They hit them with virtual hurricanes.

That provides the baseline for pricing all historic catastrophe risk across the world. But a lot of risks sit outside those two core models, that kind of act as like credit ratings, but for reinsurance. I was on the desk that handled everything that sat outside of that suite of well established, well modeled risks.

Kyla: So you handled things that weren’t hurricanes, weren’t tornadoes - just something that somebody thought wouldn’t happen?

Grant: More things that we haven't systematically modeled yet. For example,

India is an overwhelmingly rural country and it's agriculture historically has been rain fed.

They're entirely dependent on the monsoon rains that come between June and roughly September of every single year. People watch the rain pattern every single year - it's really important to the lives of a billion people.

In 2014, 2015, they had really nasty losses *but* there wasn't any national agricultural insurance scheme in place.

They decided to start one which would - overnight become tone of the biggest agricultural insurance programs in the world.

I was one of the main kind of reinsurers of that for a couple of years. I spent a lot of time in individual rural districts of India, looking at the state of crop, and then going back home and building statistical models on the basis of what we knew about how the crops grow or how the rain fell, or just how the individual insurance companies involved do or do not do a good job administering the program.

Kyla: How do you begin to build a model and price out a potential catastrophe happening, especially with regards to India?

Grant: The way that a lot of agricultural insurance programs work globally is that they're called indemnity programs.

An indemnity means that somebody shows up with a clipboard at your farm and says like, “boy, you lost a lot of crops here and here and here. And we're going to cut you a check.” That's very specific to your experience.

Now you can imagine that in the world of large American farms, that works, it still has its inefficiencies, but the scale is well-aligned.

But once you get down to Indian farms, which on average, are much, much smaller than American farms. Somewhere around 65% of the total population is rural. There's just too many farms.

So what you do is you randomly pick farms and systematically measure their yield for different crops at those randomly picked farms. Then we pay all the farmers in an area based off of those crop cutting experiments.

You end up with this data set, which is saying - here are all the crop cutting experiments, here are all the yields for all the individual villages all around India. On that basis, you can start building statistical models that link that up to rainfall at certain times of the year, or, different problems that might be tractable for data science, machine learning type techniques.

Derivatives in 2012

Kyla: You spent a lot of time in derivatives, working in the CFTC in 2012. Commodities are on a tear right now - can you talk about now relative to then?

Grant: Go back to 2010, Gary Gensler, was the chairman of the CFTC. And we had the Flash Crash, a huge intraday move, and all sorts of major indexes, futures, core individual indices seem to move in crazy ways and people were like - was it a fat finger error or what? This tells you a little bit about the bureaucratic mentality of regulatory bodies - but

Gary Gensler really wanted to be the one in front of America explaining what had just happened. There was a researcher on his team, Andrei Kirilenko

Even though a lot of the markets that were associated with the flash crash weren’t under Gary Gensler’s regulatory remit, he was the one who could come with interesting analysis of what had happened during the flash crash and why.

That started off this circumstance where the research team at the CFTC got a lot of resources to bring in outside academics, to just work on various problems.

The quid pro quo was you're going to work, supporting us in implementing and responding to questions regarding the implementation of the Dodd-Frank overhaul of American financial regulation

In return, we're going to let you work with some really interesting data

That was cool until about 2012. I was working on questions of base rates - how often do new and interesting futures and derivatives contracts actually reach sustainable level of high trading. I was working with a researcher there named Mike Penick, really smart guy who had done all this hard work of digitizing physical log books of open interest and trading volumes.

In the past, with futures and options trading, you really had to succeed or else you were going to fail. There was no in-between in terms of trading historically, like you either came right out of the gate and did extraordinarily well, like, interest rate derivatives, or you fell on your face like shrimp derivatives.

There was a lot of failures.

I always loved the story of futures on opening weekend at the box office. The film industry lobbied to kill it. And then of course, onions where the government has collectively said we will not trade futures in these contracts, in perpetuity seemingly.

I was humming along having fun, but unbeknownst to me, a lot of people were doing a lot of really interesting work in the public interest that was showing:

High-frequency traders were making more or less risk-free profits at the expense of pension funds.

It was a short window - the research might've already been stale by the time that they displayed it publicly.

They did have a public event where they showed off some of this research, it made it into newspapers.

Some of the trading venues that were supplying the underlying data said, this was not what we signed up for. Effectively, our high-frequency trading clients are making tons of money. We don't want public research denigrating them.

Overnight I was fired as a contractor, as well as all of the outside academics who are working in the department. The book Flash Boys has like a two sentence description of what happened, but it was really interesting to go from this department that was putting out really interesting research to overnight we were all locked out of the building, because of this controversial research. I think that just goes to show the difficulty of doing research in the public interest at regulators.

Broader Commodity Markets

Kyla: Just looking at the commodity market right now - what’s happening with nickel, with everything. Any thoughts around broader market movement at the movement?

Grant: One thing that you can look back at the history of these marketplaces and see that oftentimes people are using a traded commodity as a shadow, crosshedge, dirty hedge for what they actually trade in.

In corn markets, the actual traded market is a pretty good representation of what most people produce, but there's also all sorts of markets where there's a real gap between the actual commodity that is produced and the thing that's traded on the marketplace

To the extent that those gaps exist - they feel kind of theoretical in times of normalcy. But in times of crisis, when you really genuinely need this type of commodity in this type of place, that's when you see weird dislocations, like what's happened in nickel.

If you remember back to the previous big crisis in agricultural commodities, that one started in rice.

Rice is not really an internationally traded thing, but you'll recall that people really started taking note of rice price displacement. I think it was Sam's Club or maybe Costco put a limit on how much rice you could buy in. This was in 2007, 2008, when the prices were going wild.

That's another one where it's not really an internationally traded market because in large part everybody eats their own special kind of rice - basmati rice is its own market, short grain, sushi rice, etc.

There's not a lot of standardized trade on an international level between different rice folks. And it's considered, a point of national security in places like India.

Consequently there's real restrictions on import and export - that diversity within a market always leaves a market vulnerable in times of acute stress.

In the nickel case, the type of nickel that the main trader associated with the displacement was producing was fundamentally different than the type that was actually deliverable under the contract. And so that creates an opportunity for there to be short-term price displacement that you can wave functional quality difference away in circumstances where things are just normal. There's going to be a regular statistical link between the nickel that's traded on the exchange and the nickel that producer makes. But in times of acute crises where you actually have to just show up with the specific grade of nickel. Then things can go really wild and there's all sorts of futures contracts that never actually got off the ground because there wasn't enough standardization in the underlying contract because too many people trade things that are too different in terms of their underlying quality.

Like there's no tomatoes futures contract because the quality of tomatoes varies too much. We can't even get close to a circumstance where we all are looking at the same page when it comes to the price of tomatoes.

Kyla: Does that worry you? Are you like, we need to have tomato contracts or you are you like, this is just a thing that's happening and that's okay? Do we need to have contracts for everything?

Grant: I think it's the deviation from people's expectations that creates the real chaos in markets in the short term. It's when you thought you had a nickel that more or less was like the nickel that was trading, and then all of a sudden you find out that's not the case. As long as everybody's on the same page, then markets will proceed in a more or less orderly fashion. That's not always true, but first order approximation.

Agriculture Risk

Kyla: That gets into agriculture risk too. So going back to what we talked about a little bit earlier with India and wheat and broader risk - when you think about agricultural markets - cause this is so relevant right now - how do you price it out?

Grant: It's pretty similar. Oftentimes you have to think about what's baked into underlying prices and underlying expectations and then look for the meaningful gaps between what's baked in - so for example, here's one good global crop monitor for wheat.

You're looking around at different places that are producing wheat right now. Green is good. Yellow is a place to watch. One of the important pieces to note is that actually on a global scale, most of the wheat in the world is produced in China and India.

China - we never really know what's going on. There's not a lot of publicly available information on the basis of satellite information. We were thinking that China was doing well this year, but there's also been public reports that there's been flooding. Ultimately, it's really hard to understand.

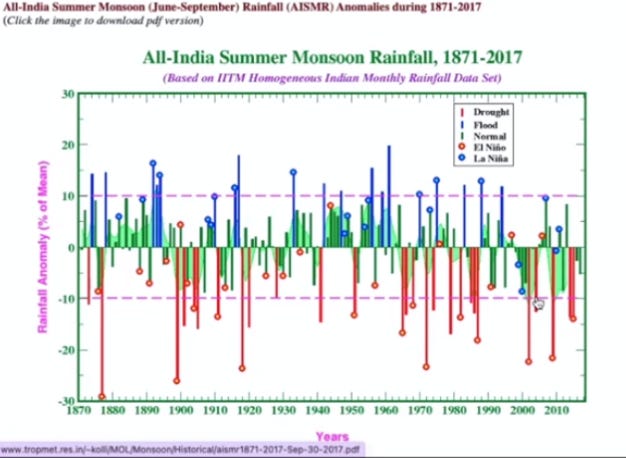

India has had a really unprecedented string of good monsoons since 2015, roughly. Funnily enough since they put up this large, good agricultural insurance program, they've had excellent monsoons, which means - as you can expect- everybody is turning around and saying like, “why did we pay for all this stupid insurance? This is a highway robbery. We haven't gotten a material payout.”

It just sort of happens that we've had a string of like five or six, really manageable monsoons in a row and on a historic basis, usually we see a lot more nasty monsoons.

So here’s a picture of Indian monsoons over time.

We just have cruised in the normal range for a few years in a row when we were assessing Indian output, which today is kind of green - that's only kind of a first order assumption and gives you a first order sense of like, How is India doing? But in practice, like a lot of our experiences as insurers or reinsurers is dictated by much more localized phenomenon that you can't really assess it at arms length easily.

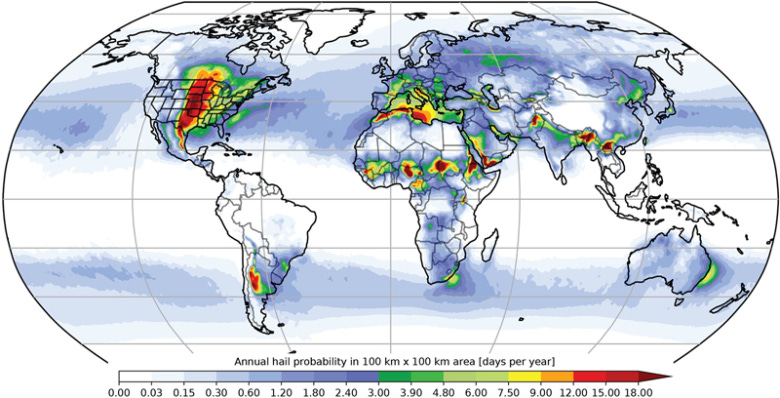

Here's a map of hail incidents globally. Red is a lot of hail and white is not too much hail. Most of India's wheat is grown right in the foothills, running up to the Himalayas, which also the right in front of mountain ranges where you get a lot of nasty hail and hail is a really tricky risk, right? Because it'll hit one town or half of a town, and leave the other half of the town totally untouched. Consequently, it was individual hail events that might stretch all across Northern India. That would wipe out huge pieces of the wheat crop, right at this time of year, that would always surprise and result in nasty losses in agricultural books. And it's really, really hard even today to assess what hail has hit your particular village or your particular field.

All that is to say it's a good circumstances for two of the largest producers and consumers of wheat in the world. But we're in a critical period for risks, like hail that could still sort of spoil the party on an, on a one-off basis.

The other piece of this is that more and more, there's been a trend because the cost of storing wheat and grains in general has gone down more individual farmers are taking into their own hands, the infrastructure to store their grains than say in the past. And so places like Australia, it's really actually hard to estimate. Individual farmers have built more infrastructure for storing their own wheat, as opposed to in the past where they they'd go and bring their wheat to a third party who owned the storage infrastructure. So as more and more people are storing more and more of their wheat privately, and information about those storage patterns just becomes less.

Those would be two areas, storage and hail, where you might see like big deviations for people's expectations right now.

Kyla: Does India grow spring wheat? Is their planting season about to commence?

Grant: India's pattern of cropping is built around the monsoon. The way that the monsoon works is every single year, right here in Sri Lanka, the monsoon starts right around June and then it just cruises up into Pakistan until about early July. That's what we're watching throughout the first part of the season. People plant as the monsoon comes through their village. You can't plant in rock hard ground. So whether the monsoon is delayed in any given year, that's going to determine the planting schedule for the first crop of the year, which tends to be really water intensive and harvest that first crop in November, December kind of ballpark. Then the second crop of the year tends to be wheat and pulses, lentils, things like that. So that would have been in the ground in December, January, and they'd be harvesting now. And at the last minute, hail events that cover entire Indian states could like wipe out a material portion of the overall crop.

Kyla: I'm a little bit interested in just the reinsurance process of that. So if all of a sudden India gets hit by a massive hail storm, what does that look like? What did that look like for you as a reinsurer?

Grant: Well, reinsurers don't really have the luxury of trading in and out of their positions, the same way that other folks do. You can't really cut your losses. If a hurricane is coming to hit Miami, I mean, there's a little bit of trading that people do, but more or less you're, you're just going to pay what's dictated in the underlying policy. That's a circumstance where you have to get a pretty good sense of what the long-term averages, adjust for factors like El Nino that you can observe before getting on the policy. And then you just sit and wait and see how things go. That's the very idea of insurance and reinsurance, it's that you can come back to the same person who you talked to originally and remind them that they have.

Kyla: I want to get a little bit into your work with scoot science as well. Are there any themes that you and scoot are paying attention to? In the commodity markets that are worrying or exciting? What are you all sort of like watching right now?

Grant: It's helpful to compare, salmon markets to some of the other markets that people might be watching today. And that gives you a sense of where we're coming from.

Electricity is a commodity market where literally for the whole thing to work, we have to consume exactly what we produce at the moment that it's produced more or less. There's no ability functionally at a utility scale to store electricity. We're working on that, but today you got to use it or lose the whole system really. You can move it across space pretty kind of easily. We build transmission lines and you can move the electricity instantly across space, but you can't really store it and move it across time.

Currency is pretty good - you put cash in your wallet, it's hopefully there when you come back. it's movable across space and across time in a, in a pretty functional way.

Water isn't traded globally, but it's pretty easy to store relatively speaking. Like we have reservoirs or underground places that we put water over time and it’s there when we go back and get it.

Then there's things that are just really expensive to store or move across space or time like services.

Those aren't really traded commodities.

So something like wheat - we're seeing the limits of it being moved across space, like in practice 30% or something of the world's wheat is exported and actually moved across space is coming from Russia or Ukraine.

It's actually much harder to move across space. It's still pretty easy to move across time.

You can store a wheat for a long time, pretty cheaply.

However, in low-income countries, there's not a lot of good storage opportunities for grains, etc.

People actually use livestock as a way to store grain in low income communities.

You can think of your goat, if you're in a village in Ethiopia, as being a form of storage across space and time, functionally.

When you see really acute periods of nasty, food insecurity, famine type situation, it's often because the exchange rate between livestock and edible food goes wild.

Everybody's trying to sell their goats all at once. There's goat hyperinflation, and all of your savings kind of evaporate over time.

Functionally, that's one way of thinking about famine.

And there's markets like rice that theoretically could be really good about for storage, but in practice, there isn't one rice market, there's too many rice markets for any one of them to really be globally traded.

Of all of these salmon, which we work on today is really actually pretty close to electricity

Most of what we consume in terms of salmon is not frozen, it's fresh. It has to more or less be consumed roughly in the time that it's produced.

We can move it from country to country. Most of our salmon comes from Norway or Chile or some someplace, but we really can't move it across time without losing a ton of the value.

So freezing your salmon instantly results in it having a lot less market value so supply in the short term is pretty well fixed. It takes two and a half years or something to grow a salmon to a commercial weight.

In the short term, the salmon haul is going to be what it's going to be. That creates electricity type displacements in the marketplace than a lot of other commodities.

I've always, always loved agricultural issues, but with agricultural markets in some cases, there is just tons of information and it's really hard to add additional value through your expertise or just the margins in the underlying crop are really low.

So how much profit your brilliant idea is fundamentally constrained because the marketplace is already pretty efficient. None of those apply to salmon. Salmon's one where a lot of the greenhouse gas footprint is driven by mortality on these farms. If we can lower the mortality, then we're lowering the carbon emission per unit of protein that we provide.

The margins have been astoundingly high, so people need your expertise and there just isn't a lot of expertise out there to go around.

I work with this really accomplished, interesting team of scientists who love the opportunity to apply their expertise, their PhD's, forecasting ocean temperatures and things like that. They help salmon companies navigate a lot of really weird acute risks that come along. The equivalent of hail type events are faced everyday by salmon farms around the world.

Kyla: How do you think about Scoot in light of this broader commodity inflation? What role do you think salmon farming - sustainable salmon farming - has in this world where things that are normally not scarce, seem a lot more scarce?

Grant: Even when you talked about this world where things normally feel scarce, you're referencing people's expectations and people's expectations are actually at this point, pretty darn efficient in the world of agriculture. Way more efficient than they were in the 1940s or 1950s, when we saw on a global scale, massive famines all across the world. Now those massive famines, it's not just about information. Oftentimes they're like a lot of government policy involved or other sorts of complicated factors but just knowing what's happening and having some arm's length way of grokking the circumstance - people just take that for granted in the world of agriculture in a way that they can't, when we come to the oceans. We have been developing tools to support forecasting of weather and things like that for decades and they're pretty good today. That's just not the case in ocean-based industries. They just don't have the equivalent of a five-day forecast for ocean conditions.

I can show you actually our forecasting tool. Here's British Columbia.

This is one of the regions that's had a lot of constraining impacts of climate change. It's not a coincidence that this has been the region that's asked for our help and forecasting ocean conditions the most.

We can go backwards and forwards in time using physics-based models of the underlying ocean.

This is the first time in many circumstances that you have something that's functionally equivalent to all the big physics-based weather models that are running globally and are a tailwind for all of agriculture, as they're trying to decide when to plant or when to harvest or things like that - that just doesn't exist in oceans today.

We're kind of the first ones to build it. So it like, it's exciting. It's cool to be able to, in a relatively simple way, connect up these oceanographers, who've been working really hard on quantitative problems, with the people who didn't even know that those tools were available.

Kyla: How do you all think about the balance of the economy and the environment? Helping the communities that rely on salmon farming, have a more sustainable path, but also make money which they need?

Grant: There are definitely environmental impacts that have to be managed that are associated with these operations. There's a lot of questions also about fish welfare and the ethical and moral considerations, the standards that you have to try and meet if you're going to feed the global population in a responsible way. So we feel like we're in a position where we're offering people the tools to actually systematically get better on all of those things. And it's worth noting that the salmon industry has had this tremendous success story in a weird way.

When I first read about this industry there's a big Nature article and I want to say 2001, 2002, that was saying basically salmon is hopeless and salmon will never, ever successfully be a protein source that actually on net is supporting sustainable, seafood consumption. So much of the feed at the time that was going into salmon was coming from places like Peru, where they would harvest anchovies, turn them into fish meal, fly them or ship them halfway across the world and feed them the salmon. And at the time, their regime for feeding the salmon, wasn't very efficient. It was taking more than a kilogram of fish input to produce one kilogram of fish output. But at the same time, I mean, there was a major driver, which was the world's fish stocks were plummeting. A lot of nature places all around the world had reached the point where they'd successfully over fished. And fast forward 20 years later, that ratio of the feed efficiency has changed dramatically to the point where salmon is now on net creating fish and that's all with the basic tools that we take for granted in agriculture. So I just see such a great pathway for groups to continue to improve, and they really want to. I would bet that there's no other industry in the world that has a higher percentage of the total industry, that's already signed up to green loan facilities or green bonds where they're pledging the, at these specific metrics, we're going to get better over time.

So we'd like to help them do that as quickly as possible.

Kyla: I think it's a super needed. Because we have all this ESG talk and sometimes that doesn't translate to real world application. I think you're making a lot of progress.

Grant: Thanks. I mean, I just kinda love these problems, so it doesn't feel very like, but I will say, you know, there are some illustrative stories that resonate in my mind as I'm thinking about some of the issues related to salmon today and the challenges that it's facing. Being an agricultural weenie, I went to college in Washington, DC, and there's this great international think tank that's focused on agricultural issues.

At the time, there was a researcher who had dedicated his life to plant breeding on behalf of kids in Asia who had low vitamin D. A lot of rice doesn't have vitamin D and there are systematic nutrient deficiencies among low-income communities, all across Asia, who rely on rice for a big portion of their total calories.

He was working on genetically modifying rice so that it would produce vitamin D and a lot of kids wouldn't suffer from the blindness associated with vitamin D deficiency. And at the time, you know, GMO crops were so controversial and it just made a huge impression to me.

Just seeing this dedicated rice breeder who had put his life's work in a very earnest way in helping the world. And it felt like there was a lot of pushback against the technological package in which those good intentions and success arrived. It's kind of a really tragic story that these products were never really commercialized a large part because of controversy related to the various labels that were put on the effort itself. Just to hear him talk about the vision he had was really inspiring and also a little heartbreaking. That helps frame some of the work that we're doing today, even on a, at times, controversial, section of agriculture,

Kyla: Is there anything else that you want to add or any final thoughts that you have?

Grant: I'll leave you with this. There's so many interesting stories that are just not covered in the world of agriculture. For example, in 2019, some people estimate that something like 40% of all of China's pigs died from African swine fever, which was this terrible, massive pandemic that swept through the pig population in China. We don't really know what those overall numbers were, but it paralleled with the subsequent pandemic that we suffered as humans - pigs and humans have a lot of biological similarities.

Just seeing this pig pandemic playout - functionally such a huge portion of all sentient beings on the planet died in this pandemic and it never even was mentioned in newspapers. That seems crazy to me. I feel like agriculture is just filled with those fascinating, interesting stories that reflect back on the lives of human people who aren't from rural areas. Periodic commodity crises are opportunities at least to remember that that there's a lot happening in the world's communities. Even when we can go 10, 15, 20 years collectively not paying all that much attention.

Check out ScootScience here!

Disclaimer: This is not financial advice or recommendation for any investment. The Content is for informational purposes only, you should not construe any such information or other material as legal, tax, investment, financial, or other advice.

One of the most fascinating interviews I’ve read in a while. Great stuff!