Q&A: Wealth Concentration, the 1970s, and Stagflation

things are different but they aren't

Joey and I answer some questions around wealth in crypto (and fiat), supply shocks, and NFTs!

If you’re already subscribed, thank you! If you would like to subscribe, please do so here:

⭐️A quick housekeeping item - if your company would like to partner on a project with me, please fill out this partnership form!

This post is partnered with Joey Politano, who writes a very good newsletter (which you should subscribe to)! Over the last several weeks, we’ve been collecting questions from readers. Today, we’re finally answering the best ones—with a twist! Half of our answers are posted in my newsletter, and the other half are posted in Joey’s newsletter below:

Be sure to check out Joey’s post where we discuss the Fed’s independence, the housing bubble, Fed lessons learned, and more.

Is BTC/ETH/crypto wealth too concentrated?

Kyla:

Wealth concentration is everywhere: So this is an interesting question, because then you have to ask - is fiat wealth too concentrated? Like maybe, right? Just look at the graph from Statista below - the Top 1% are moving and grooving - their wealth has increased from 23.5% of net wealth to 32.1% of net wealth from the beginning of 1990s. And inflation hits lower income consumers the hardest - so the disparity really isn’t improving, in fact, it’s most likely getting worse. Corporate stock ownership is a large reason for wealth concentration, and that’s mostly concentrated in wealthier individuals too.

Source: Statista

Crypto was sort of meant to be the solution to this. Satoshi set out to create a peer to peer network that was focused on removing intermediaries, with the goal to create less wealth leakage to middlemen. The original cypherpunk movement was around this idea of freedom - including economic freedom. But does crypto *now* do all that? It has the potential to, definitely. But there are so many questions - what exactly *is* Tether, what exactly are the 0.01% of bitcoin holders doing with 27% of the bitcoin in circulation, when will NFT projects stop being massive rug pulls etc?

I think the research paper from Sai, Buckley, and Le Gear does a good job diving deep into different ways to analyze wealth inequality in the crypto space - with the ultimate conclusion being - “yeah, this sort of is skewed, but (for example) Bitcoin has the same Gini value as Australia and Dogecoin which is one of the most unequal (!!!!) has the same Gini value as the US - so yeah, there’s some wealth inequality in crypto but not any worse than what we already have” - crypto isn’t equal, but it isn’t any less equal than what we are currently dealing with.

Joey:

The short answer is that crypto wealth is so concentrated that it threatens the long term functioning of a lot of the crypto ecosystem, but not so concentrated that it will cause imminent collapse. Reliable numbers are hard to come by due to the pseudo-anonymity afforded by cryptocurrencies, but Igor Makarov and Antionette Schoar estimated that the top 0.1% of Bitcoin owners held 30% of all Bitcoin (for comparison, the top 0.1% holds 18.6% of total wealth in the US as measured by Piketty, Saez, and Zucman in 2018). This hasn’t been that big an issue because the share of a cryptocurrency’s market cap needed for network usage is small, but whales do have an obvious outsized influence in the crypto ecosystem. They can push crypto intermediaries, miners, or validators to act on their behalf. They can use their social media clout to drive prices up or down at a whim. They can design carve outs for smart contracts or drive consolidation among platforms. The Ethereum network’s only fork was basically created because whales were scammed out of their money and wanted it back—that’s not a power most crypto users have.

Things are also likely to get worse. For one, newer crypto projects are giving a larger share to insiders before going public. For two, the basic structure of crypto promotes growing wealth inequality. Crypto wealth, like most wealth, tends to compound on itself—a process made all the worse by the deflationary design of most coins. Since most coins are designed to increase in value dramatically during the growth phase and steadily thereafter, it becomes harder for late-comers (say, the children of today) to enter the ecosystem. I worry that the future of crypto resembles Axie Infinity, a “play-to-earn” crypto game where owners outsource the actual “playing” to contract workers in the Philippines and other low-income countries at rock-bottom rates.

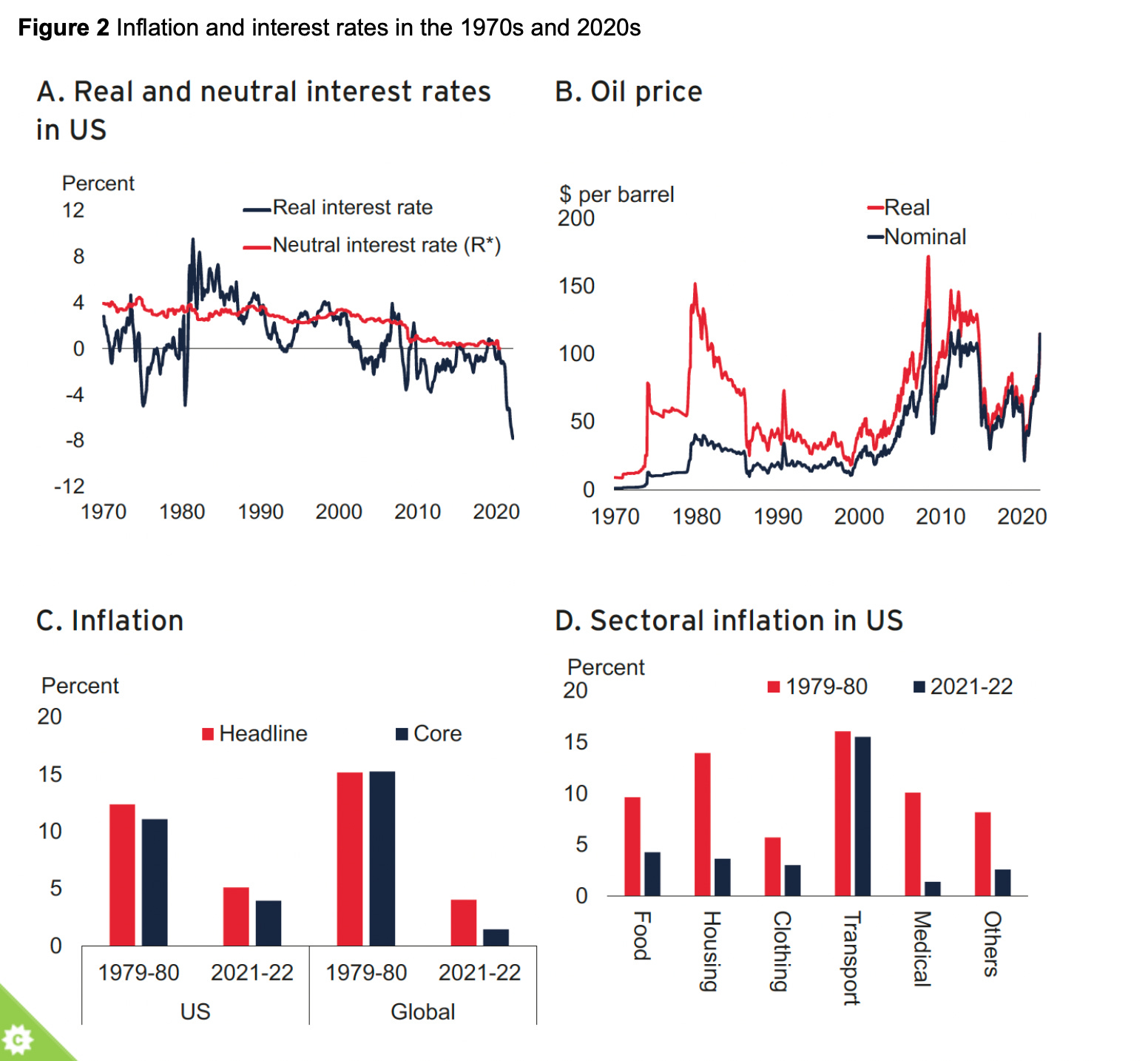

Is this similar/different from 1970s?

Kyla:

It’s different: There is a good Odd Lots podcast on this (a sentence I probably say once a day at this point) with Viktor Shvets. I think that the points he makes are pretty salient - the world is massively different now versus the 1970s, the labor market is completely different, asset prices are completely different. We have massive wealth inequality now, to circle back to the previous question on crypto. But we also have a raging war, commodity shocks, skewed demographics, inflation without much wage growth - and that’s worrying.

But it’s also similar: But yeah, we’ve had huge spikes in commodity prices which was one of the defining components of the 1970s. In the 1970s, OPEC put an embargo on oil exports, which of course caused a huge supply shock in oil and led to huge price increases (prices literally quadrupling). It was compounded by easy monetary policy (which sounds familiar). All of that led to stagflation, which is literally a curse word in modern parlance. “Low growth, high inflation”, a tough storm for any economy - so things got Volckered - interest rates spiked, the economy shrank, *buuut* inflation was sharply reduced.

But now is different than then. We have supply-side inflation which should ease (however, China’s COVID is concerning and the war continues to rage), and the jobs market is really strong. So things are okay - but there’s definitely risk that things could not be okay - which is why we are seeing an aggressive Fed (and Bullard thinks this Fed is more credible than the 1970s Fed)

Europe: However, it’s also important to note that Europe is more exposed than the U.S., because they are so reliant on energy imports from Russia, Belarus etc - which is concerning. And to note, this is not close to being over - largely, these energy worries have just begun.

Also there is a lot of debt now - and debt servicing costs are going to tick up as rates tick up too, which isn’t 1970s-esque persay, but important.

Joey:

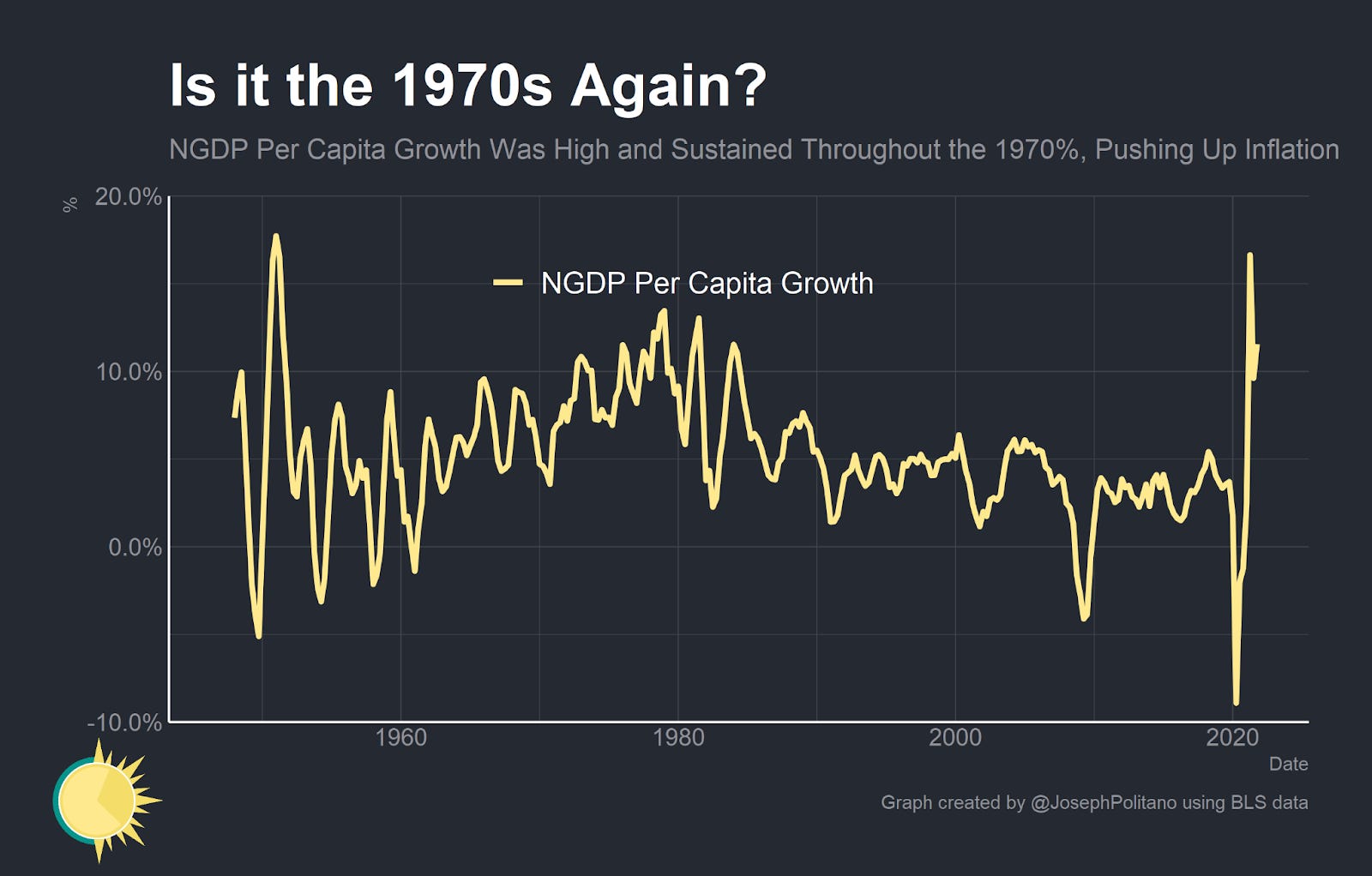

Humans are hard-wired to seek patterns and to communicate information through narratives, and that leads us to always search history to understand current events. But this often leads us astray, as the future rarely conforms to the past and historical patterns are just as often noise as signal. The similarities to the 1970s are obvious: high inflation, an energy crisis, and geopolitical conflict. But I think there are far more differences than similarities.

The labor market of the 1970’s “stagflation” was shaped by high growth in working age-population and elevated unemployment. Today we have low unemployment and low working-age population growth. Gasoline and energy goods made up 6% of total personal consumption expenditures in late 1979 against only 2.5% today, and the US is no longer a massive net importer of oil. Inflation in the 1970s persisted partially because central bankers had little understanding of how to control the pure fiat money regime they had created, leading them to allow nominal per-person spending to grow at 10% a year for nearly a decade. Today’s federal reserve has greatly refined their understanding of the macroeconomy—which is why they are tightening policy now

How do you square rising commodity and NFT prices?

Kyla

The Mint mints: Rishi Sunak, the chancellor of the Royal Treasury in Great Britain, asked the Royal Mint to create an NFT. It went over really badly with the public - the whole thing was to focus on making the U.K. a crypto hub but, “maybe not right now” seemed to be the general consensus of the people considering that there is a global energy crisis and it just felt… misplaced.

Polarization: And I think that’s sort of the general public’s vibe around crypto - I personally think it is a good and important idea for governments to explore cryptoassets - but I’ve written before on how polarizing crypto can be. I think its also important to talk about some of the disparity in prices - it just feels weird to see people spend millions and millions on the monkey pictures when so many can’t even afford stable housing.

Expensive: So I think it actually sort of circles back to the wealth gap in crypto (and the world). There are the haves and the have-nots, as there has always been. Sometimes it feels like that the haves are telling the world to eat cake, you know? And crypto is a useful tool for developing AND developed nations - but is also is really difficult to have disposable income to play around in crypto if you can’t afford gas because oil prices have mooned - and if you can’t play around in crypto, you can never make the gobs of money that some of those in the ecosystem have made.

So I answered this sort of backwards and roundabout but basically - people seek safe havens during times of volatility (NFTs can be that to an extent?) - but rising commodity prices are really important and supersede everything. Food access and energy supply are the common denominators to every human. And it’s important we allocate resources and capital to that *and* web3.

Joey:

Today’s economy needs a wealth of physical, hard-tech investment to meet the climate emergency and lift people across the world out of poverty. In part, today’s high commodity prices reflect that need (alongside a strong macroeconomy after a decade of weakness, the increased demand for goods caused by the pandemic, and the supply shock caused by the Russian invasion of Ukraine). Spending on NFTs doesn’t necessarily compete with that necessary investment. After all, few people would claim that all Disney+ subscriptions represent wasteful spending even though (as with NFTs) the core transaction is hard cash for infinitely reproducible digital media. That’s because the manufactured digital scarcity (barring piracy, you have to pay Disney in order to view their content) of Disney+ generally incentivizes the creation of positive economic goods: Disney spent $25 billion on content last year and created a host of widely beloved shows and movies in the process. All property rights, physical or digital, are social constructs designed to incentivize economic production, and high prices can incentivize property owners to invest in additional production.

The problem with NFTs isn’t that they are pricey objects of manufactured digital scarcity, it’s that the structure of digital scarcity in crypto incentivizes the wrong kind of production. Abundant copying and ease of piracy has caused dramatic underproduction of entertainment, artistic, and information goods over the last 25 years, but NFTs do little to address this. NFT prices aren’t correlated with entertainment or artistic value, they are just tenuously connected to popularity through the possibility to profit from resale. The result is that very few NFT projects are anything more than tokenized versions of AI-generated jpegs with stellar marketing teams. Underpinning that system is many more programmers and several orders of magnitude more energy consumption than an equivalent crypto-free program would need. The goal of digital scarcity should be to incentivize productive work and investment in the digital realm in the same way commodity prices incentivize productive work and investment in the physical realm, but NFTs have so far failed in that goal. I’m skeptical that NFTs will ever achieve that goal in a more efficient way than simple paywalls or microtransactions could.

What is your advice for students?

Kyla:

I had a nonlinear path (kind of) to where I am now. I had a finance blog in school, wrote for Seeking Alpha, traded options - I was iterating on finance before I was ever in the “real world”. But I also sold cars, did research internships, etc - I basically wanted to keep all my options open for everything. I chose my first job at Capital Group because it was a rotational program - it wasn’t going to be one job, it was going to be a new job every 3 months. When I left Cap Group to join a tech startup, I was mostly just trying to find my footing after realizing that I had to follow my heart - which involves both education and creation. So my advice would be:

Remain open - talk to as many people that you can, do as many things as you can, and don’t let fear dictate what you do/don’t do

Don’t give up on yourself - I came from a nontarget school, had no network, knew nothing - you have to be your own biggest fan

Never underestimate the power of questions - Ask a lot of things from both yourself and the world. Remain curious - finding things interesting is very different from applied curiosity. Explore as much as you can.

Joey:

I get asked this question a lot, and to be honest I am always intimidated by it. Unlike Kyla, economic analysis is just a passion project for me—something I do often but doesn’t pay me a dime. My day job is completely unrelated to the things I write about in my blog, so it’s not like I “made it.” I still consider myself an aspiring economist, nowhere near a real economist. So discount what I say a bit, but here’s what I would say to someone in high school or college.

First, stay in school. All the documented evidence is that extra years of schooling have immense positive effects no matter what you do (my favorite fact on this is that 1930s mobsters who had more years of schooling earned more money through criminal enterprise). “Learn to code” is trite advice because it’s good advice, so here’s what I’ll add: learn to code by repeatedly iterating on something you’re passionate about. I’ve learned more of the programming language R in 9 months of writing Apricitas than I did in 4 years of college because I was passionate about doing better and better things for Apricitas in a way I never was for college classes. Finally, consciously build a social support network: search for people who will care for you, support you, and challenge you to be better. Spend as much time as physically possible with them.

What your hottest take that doesn’t have to do with finance or econ?

Kyla:

I’m going to do this in two parts.

I think that humans are really beautiful and lovely and amazing - there’s so many cool things that we do, like build and love and create. Sometimes humans really suck (usually clouded by money or power or whatever) but most humans are really good people.

On the flip side of that, I think that we are all really sad and it’s only going to get worse. I don’t know what to make of it - but I truly think social media has erupted a part of us that is meant to have empathy and love, and skewed it to anger.

I think that we have a passion crisis where people feel completely disconnected from the world, and that’s largely because we don’t spend enough time *in* the world. I think that everyone does have a passion, but we historically haven’t been encouraged (or supported) to explore it.

Joey:

Hockey is the best spectator sport out there, and it’s not even close. The game has much better flow than the interruption-heavy sports like baseball, basketball, or (American) football but keeps higher tension than soccer due to the increased frequency of shots on goal. Power plays are far and away the best penalty system out there, striking a careful balance between punishing teams for breaking the rules while preventing referee decisions from determining the outcomes of games outright. Allowing fights helps regulate players’ in-game conduct while creating intense personal and team rivalries. Playoff upsets are reasonably possible (unlike in the NBA) but bad teams aren’t eliminated for one bad game (unlike in the NFL).

Thanks for reading everyone :)

Some Good Links

Dudley discusses stock market get rekt: If Stocks Don’t Fall, the Fed Needs to Force Them

So does Zoltan: This Is Zoltan Pozsar's Vision For Bretton Woods III

What’s the housing market doing? Mortgage Monitor February 2022

Oh sh!t: No poop for you: Manure supplies run short as fertilizer prices soar

JP Morgan and the future: Jamie Dimon’s Letter

Also relevant: JPM Guide to the Markets

The Fast(ish) and Furious Fed: Fed Officials Weigh Shrinking Balance Sheet by $95 Billion/Month

Disclaimer: This is not financial advice or recommendation for any investment. The Content is for informational purposes only, you should not construe any such information or other material as legal, tax, investment, financial, or other advice.

| A guest post by

|

Enjoyed the hot takes. Kyla's reminded me of the intro to the last newsletter. Appreciate the insights!

Thanks, fantastic reflections.