The Commotion in Commodities

bitcorn

This is a thought piece around commodities (I post daily to TikTok). I publish these once a week (beta phase), as well as single stock pieces (1-3x a month) and macro deep-dives. I also publish on TikTok, Youtube, and Twitter!

The YouTube version will be linked here:

Commodities Wyd

Commodities are on a tear right now - rapidly rising in prices on the backdrop of reopening demand, policy pressure, and supply chain issues.

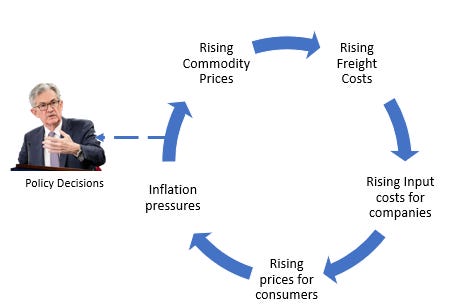

This creates the commodity price loop:

Rising commodity prices lead to rising freight costs, leading to margin pressure in companies, which eventually gets passed off to consumers - resulting in inflation. The Fed has a role in policy making here - “bottlenecks vs substantial further progress” but there are structural issues that are causing pain in the commodity space.

What’s going on in industrials?

The price increase is all about supply and demand (and structural supply side logistical issues).

There is a lower base to compare to - right now, any level of inflation is going to seem “high” because we were in lockdown for most of last year

Supply pressure overseas: COVID-19 worries in developing nations, protests, and policy implications could all put upward pressure on prices

Loose monetary policy, weaker USD, and other green infrastructure policy decisions

Reopening demand: People are going to demand goods and services.

Companies have been stagnant / reduced production for some things over the past year - and keeping up with the surge in demand is not simple.

The big question - are commodities surging because of structural production issues or because of reopening demand? If it’s from production and other long-term pressures, inflation won’t be transient. It will have to show up in prices, which leads to the feedback loop above.

Metals: Pricing Pressure from Supply Demand Mismatch

Copper is on a climb: Copper is a key component in electrical wiring, the EV boom, the broader renewables demand, all buoyed by $2.25T Biden’s infrastructure plan.

Copper is also considered a bellwether for the economy - so it makes sense that an expected GDP growth number of ~7% would cause an uptick in copper prices.

Aluminum, palladium, zinc and iron ore also on a tear

More upward pressure from reopening as well as production constraints alongside exploding demand

This is backlit for Biden’s infrastructure plan and reopening demand - more people demanding commodities. The (announced ) transition to green energy is putting upward pressure on prices too. Backstopped by supply chain issues and logistical problems, prices are at the intersection of not enough supply and too much demand.

What’s going on with agriculture?

This is the Dow Jones Commodity Index.

A similar story for what’s happening in metals is also playing out in agriculture - upward price pressure on commodities due to supply chain constraints, production issues, and demand.

Inventories are down and planted areas are low. Weather hasn’t been great with worries of drought in the US and dryness in wheat-producing countries. China has demanded a lot of corn (feed for their hogs) as well as input in other food products (sweeteners, fuel ethanol, etc)

This is creating the Bitcorn effect. Corn has gotten so expensive that it has surpassed wheat in price, a pretty rare (and concerning) occurrence

And can’t forget about lumber:

More people are demanding homes (and renovating those homes) - so lumber demand is very high

One of the main problems is sawmill capacity (amongst other things) - they’ve got the stumps, but turning that into lumber is an entirely different thing.

There are supply issues too - fires, bugs, etc - all biting into capacity.

Listen to this piece with @LumberTrading on Odd Lots for more lumber insight

Freight Rates: Higher Prices Trickle Down

Dry Bulk Shipping has ticked upwards due to the commodity price boom too. BDRY ETF is the top performing ETF of the year.

This is from one of their weekly updates -

Although the price of iron ore does not directly impact the price of freight, the economics of iron ore production and trade does indeed affect traders’ behavior, and thus freight prices - Breakwave Advisors

Behavior is driving prices.

The increase in input prices will puts pressure on everything. This is another signal of reopening demand and the shipping cost to transport commodities. Container shipping has increased in price too - as an unintended consequence, a lot of shipping containers are falling into the ocean from being stacked so high.

And we all know how important shipping is -

{kind=link}

Higher Input Prices = Higher Product Cost

Higher prices bleed into companies - if input prices rise, their profit equation gets squished. Higher costs = less profit. And a lot of companies are beginning to take note:

Companies have two options with higher prices:

Pass costs off to consumers - this is not ideal, because consumers will substitute the product for something else (buy generic toothpaste rather than Colgate) depending on the elasticity of the good

Shrink product / cheapen production - this is also not ideal, as consumers will notice overtime (Shrinkflation)

According to the FT, “The National Association of Manufacturers found that 76% of its members saw increased raw materials costs as their biggest challenge in 2021.”

Upward pressure from commodity prices will bite into profit margins - and those costs will eventually have to be passed onto consumers. And from an investing perspective, weaker profit margins will impact quarterly performance - which could impact stock prices.

What does it all boil down to?

Inflation? Underinvestment in production? Supply-side monopolization? All three?

Supply-side issues

Joe Weisenthal made the excellent point that we are at a weird point in the boom-bust cycle

People are reluctant to expand supply, and a lot of the problems are stemming from lack of supply.

So it is creating a loop of higher prices - lack of commodities pushes prices higher, lack of investment in expanding capacity to increase supply pushes prices even higher.

Underinvestment in Production

Redbuckman has a good thread on supply being a step function - you can’t just produce more copper - you have to invest in an entirely new production facility, to produce a LOT of new copper.

So producers have to be really careful - commodities are not that profitable to produce (most of the time) and can be very price sensitive.

General Inflation

Supply and demand is always the answer.

The rally is a mix of a lot of different variables- but mostly the commodities are “outperforming” any fund on the market (besides crypto, which is an entirely different discussion).

Another closeup of the performance of commodities over the past year:

So what are policy makers to do?

Right now, it’s a fine balance between logistical issues on the supply side and outsized demand from reopening pressures, infrastructure planning, and a myriad of other variables. So the Fed has two options:

Continue to say it is all transient and that things will even out over time (temporary inflation to be replaced by long term deflation)

Or say that inflation is not transient after all, and that they might have to raise rates sooner than expected (which is what has been priced in) but that could spook the markets (they hinted at this today)

Logically, a lot of the commodity price pressure is out of the hands of the Fed. They can raise rates, but that won’t fix long-term supply chain problems (it might temper the demand for homes, but Jerome Powell can’t make corn out of thin air).

Mostly, this will be watching the markets - if capacity expands, that will alleviate pricing pressure. We need do need substantial further progress. But in the meantime, bitcorn is one of the best performing investments of the year.

Job candidate: So I would like to be paid double what you are currently paying your employees.

Employer: There seems to be a misunderstanding. We just want you to work 40 hours a week for the rest of your life. It's not like we're trying to buy LUMBER.

Job candidate: * *

Employer: But hypothetically speaking, do you know where I could buy some cheap lumber? Asking for a friend.

Job candidate: * *

Nice recap! I wonder how much of this will resolve itself when/if we get clarity on the infrastructure bill. If there is a guarantee of high government spending & construction for the next 4-8 years, that should encourage immediate investment in production right?