The Great Balancing Act

on CPI, Evergrande, Russia, and crypto regulations

The balance of the markets.

If you’re already subscribed, thank you! If you’d like to subscribe, please do so here:

YouTube/Podcast up tomorrow

Topics covered this week on Everything You Need to Know

Will Russia Invade Ukraine? (w Ben Wheeler *who now has his own substack!!**)

What actually is the CPI print?

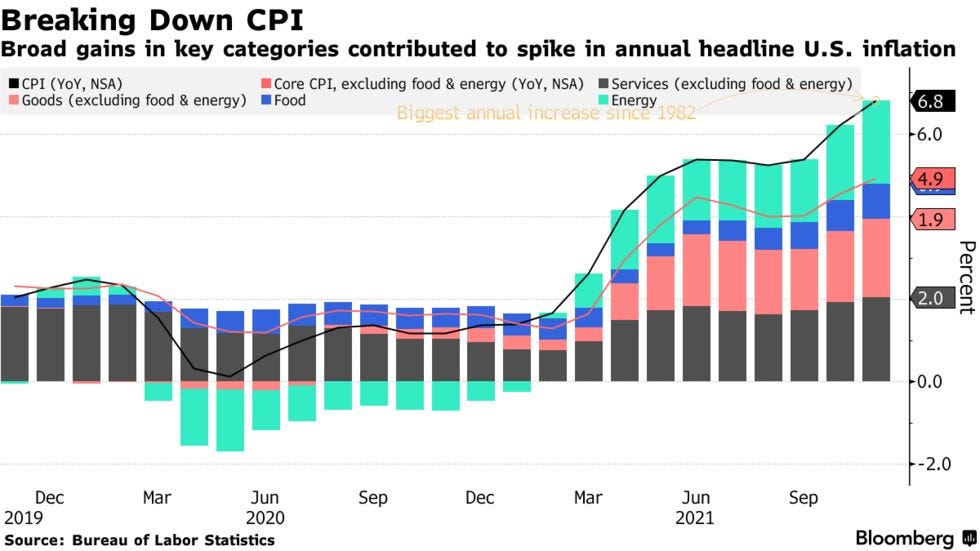

The CPI came in hot today, but at consensus levels (which means that things aren’t that ~dire~ but note, it’s definitely still spicy out there). Supply chains are still wack, and companies are just like “eh, time to pass this cost off to the consumer”. People keep saying that this is the hottest since 1982 - and of course it is.

The Numbers

CPI rose by 0.8% in November, which pushed us to an annual inflation rate to 6.8% - coming in a bit hotter than expected

Core inflation - CPI excluding food and energy

Rose 0.5% month over month and 4.9% over the past 12 months - both of these came in at consensus, so no big surprises

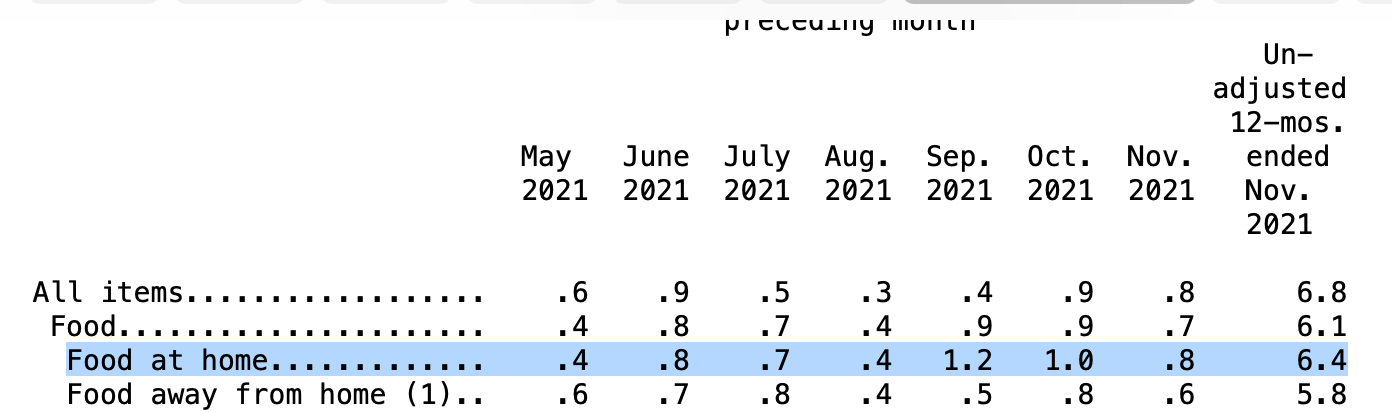

Food rose 6.4% from a year ago, the most since December 2008

An interesting thing here is that groceries (food at home, increasing 6.4%) are increasing faster than restaurants (food away from home, increasing 5.8%)

Energy prices +3.5% and Gasoline prices +6.1%

Energy was driving a lot of the CPI gain - but prices have abated since the increase in November (+4.8%) and should ease a bit more because of:

Biden tapping into the Strategic Petroleum Reserve

OPEC+ has *almost* agreed to increase production

Prices for used cars and trucks +2.5%

Used cars are driving a lot of the movement here, and this will likely abate over time

As you can see in the graph below - vehicles were driving a LOT of the movement in CPI at the beginning of the year, but that impact has reduced over time

Shelter inflation rose 0.55% from October, and 3.84% Y/Y, up from 3.38% in October, highest since 2007

And to note, this makes up ~30% of the overall CPI print and ~40% of the Core CPI print

As we see the housing market absolutely explode, this will put upward pressure on rents too - this is one to watch

Inflation is likely going to get worse before it gets better.

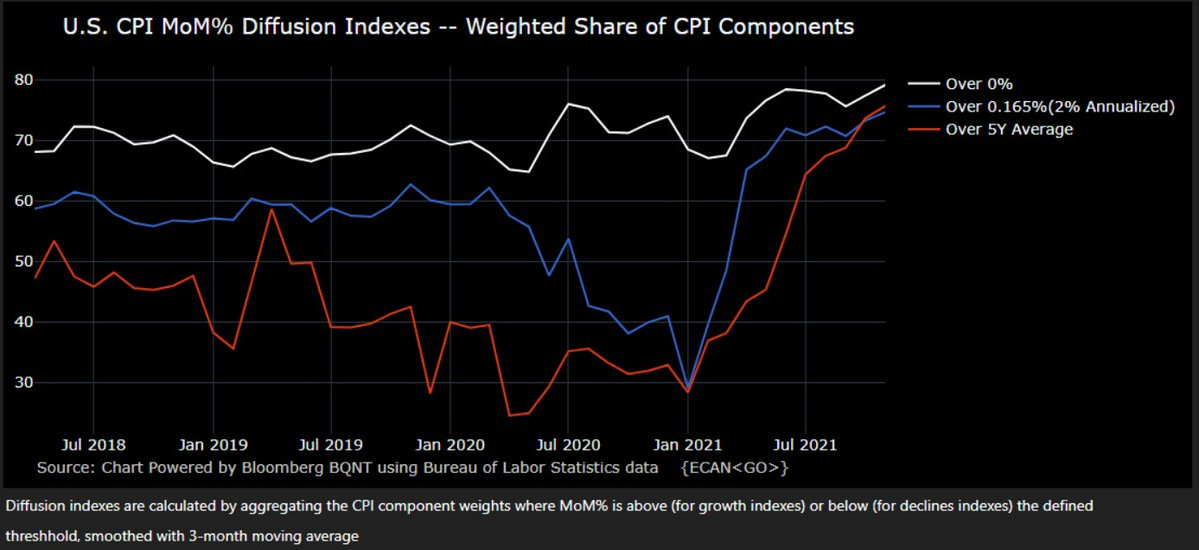

We saw a broad-based increase in most metrics, and the ones that consumers are most worried about - and it’s painful to have prices increase while wages remain stagnant. There are price increases across the board, it’s not really driven by any one component (beyond energy)

In the chart below, the sub-components that make up 75% of the CPI are *all* increasing at an annualized rate > 2%.

HOWEVER, a lot of people think that inflation has essentially stopped accelerating - it will still be high, but it won’t be increasing at an increasing rate.

Remember, we live in unprecedented times (the joy). So with the current dynamic that we are experiencing it kind of makes sense that inflation is high - we have the perfect storm. It’s definitely NOT a good thing, which is why hopefully monetary policy tools can relieve some pressure - but broadly, inflation makes sense.

It’s because of broken supply chains, a strong economy with consumers that are feeling very spendy (especially for homes) and a labor/wage shortage. When you combine all those things into one basket, it’s EXPENSIVE.

What’s the Fed going to do about that?

Well, remember the Fed really only cares about PCE as their inflation metric. However, BECAUSE CPI technically came in at consensus at 6.8% annual inflation, it could provide a larger window of time for them. If CPI had hit 7% annual inflation, that could have been a lot more reactive.

The consensus drives the narrative: Because things came in at consensus levels, there could be hope in the market that the Fed doesn’t try to come out with a hammer swinging towards higher rates as quickly - as evidenced by swaps below.

However, despite that: The FOMC is likely going to use this as a chance to continue on with their plan of tightening monetary policy at the FOMC meeting next week - raising rates, but the big question is how *fast* (which is why the SEP is important - how many rate hikes are we talking here?)

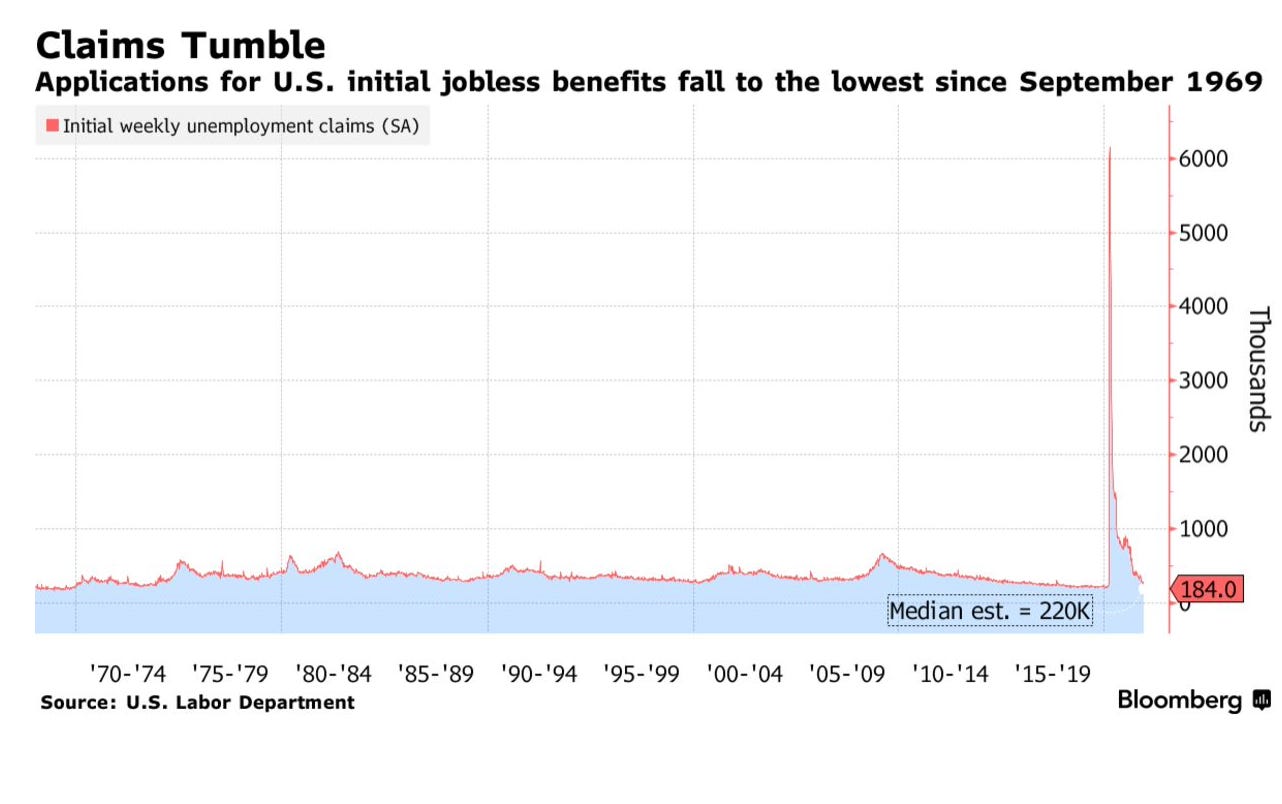

With the hot CPI + the booming jobs report yesterday (11 million! open jobs), the Fed is seeing recovery in their dual mandate of price stability and maximum employment (sort of - the labor market is funky because people are quitting, jobs are hiring, but not a lot of people are participating, but also claims are low… labor/wage shortage continues)

So the Fed has their tools:

Tapering - they are going to have to slowdown their buying of assets (probably to $30b reduction), which is largely priced into the market

Tightening - raise rates - THIS is the one to watch out for. Will we get 3 rate hikes in 2022? 4 in 2023? How angry will this make the market? Can the market even stomach higher rates at this point?

What actually counts as performance for indices?

This is an important thing to look at when considering the market from a high level - because of core drivers of things (such as the CPI and energy) a broad metric can easily be driven by those big movers.

Gavin has been doing a lot of work breaking out the actual performance of the stock market - and if you remove the core components of the Nasdaq, the index that tracks tech stocks - (AAPL, MSFT, GOOGL, TSLA, and NVDA) you can see that the Nasdaq is only up 5.79% without them. This begs the question - what is the stock market actually doing?

Is the stock market even the stock market without Apple?

What actually is Evergrande’s default?

I’ve done a fair amount of work analyzing Evergrande, and did a YouTube video breaking down their whole deal - but essentially, this company has been in deep trouble for a long time. What happened here -

Beijing has decided that overleveraged companies (like Evergrande) are no longer appropriate, and has made it very clear that debt-fueled growth is NOT the way to go anymore

So they implemented regulations in order to curb the massive borrowings - but this got in the way of property developers like Evergrande

However, there is an ecosystem here. Local governments rely on property developers like Evergrande to come in and buy up land - that is how they make their revenue. But if Evergrande can no longer have debt-fueled growth, and thus no longer buy their property, local governments have to get crafty.

They implement something called Local Government Financing Vehicles which essentially allows them to 1) put land up for sale 2) borrow money from a bank 3) buy that land back from themselves and 4) count that as revenue. This results in a LOT of hidden debt in the China’s system

Now Evergrande is getting squeezed on both sides - Fitch declared them in technical default (essentially meaning that they are failing to meet payments and are under watch) and now they are going to need to restructure before they *formally* default.

It’s really like watching a slow moving train crash - everyone knows that $300bn in liabilities is going to be *very* tough to offload, especially in Beijing’s new regulatory framework. It’s a domino pile, as Tracy Alloway highlights from Isabella Weber’s piece below - “The forest of Chinese's financial system may be burning bright in certain areas, but it's still tough to see all the trees.”

It’s a balancing act between making a point out of Evergrande (do NOT take out this much debt, other companies) and protecting their system from contagion (if Evergrande fails, people don’t get paid, empty buildings, lost jobs, etc…). Everything is a tightrope.

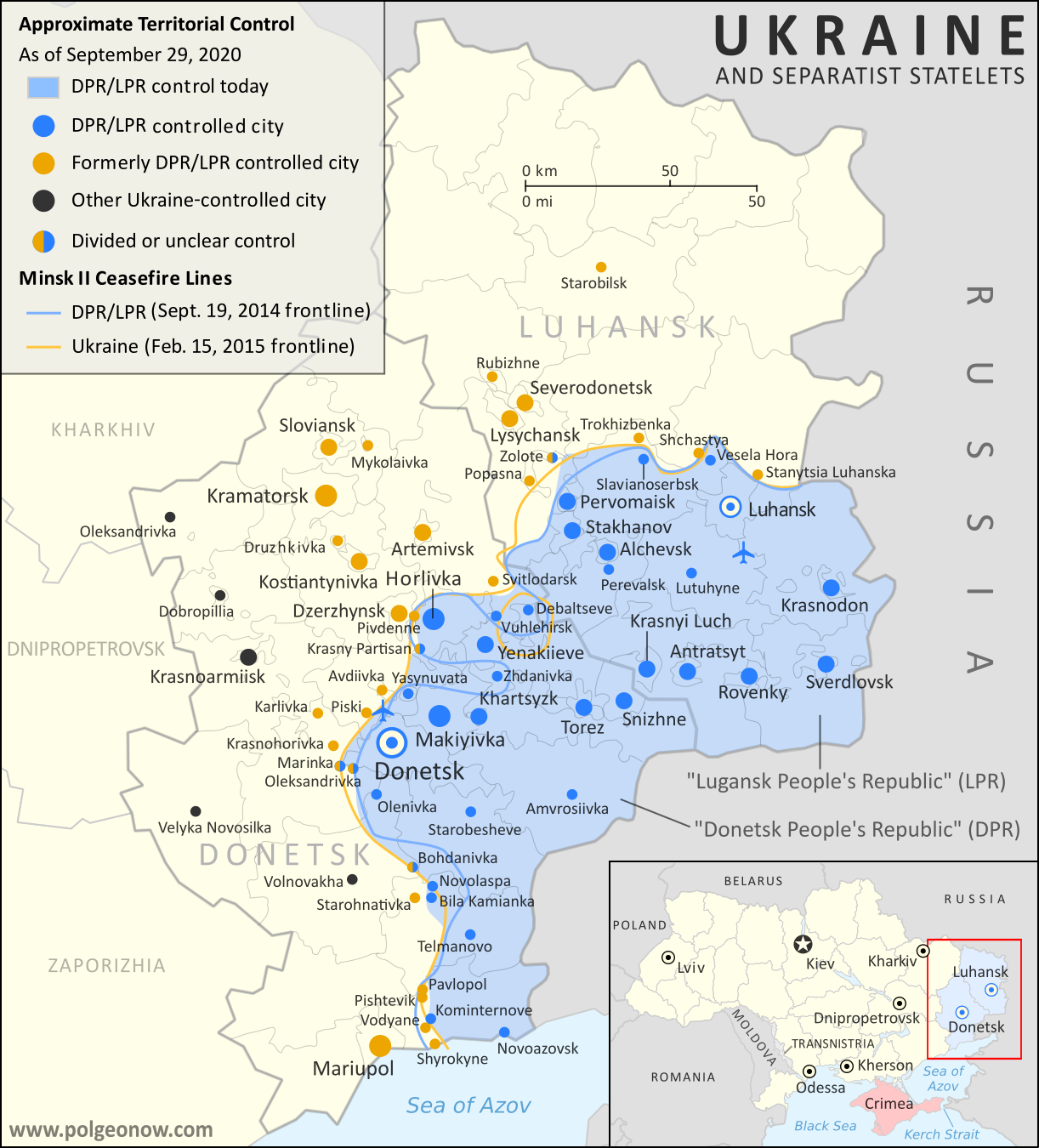

What actually is going on in Russia?

Ben and I dove pretty deep into this topic on Thursday, but here we see narrative once again. Putin wants to get the Soviet Union back together - putting geopolitical relations on thin ice. So it could be an interesting few months. As Ben outlined in his piece:

Possible Actions Taken by Russia:

Russia backdowns - this has never happened ever.

Russia gets what it wants and the EU and NATO agree to allow Ukraine to be subjected to Russia’s mercy - this is unlikely

Russia invades Ukraine to the Dnieper river, essentially annexing all of Eastern Ukraine - this is more likely

Russia doubles down on separatist forces in the Donbas.

Russia has already invaded Ukraine in the Donbas region and by doubling down, they can annex the area with plausible deniability. (Not really, everyone knows it’s their soldiers not rebels).

Russia invades Ukraine fully → “Russia is not invading Ukraine, it is threatening to launch a renewed offensive to expand it's occupation”

This would prompt a NATO response. It has to - otherwise - it endangers the security of Eastern Europe.

{kind=link}

{kind=link}

Just as a note, Russia is a very, very big part of the energy market worldwide. This goes without being said, but the consequences of them fully invading Ukraine would be a shockwave across the world.

What actually is crypto regulation?

So, mongoose coin right?

Crypto leaders testified in front of Congress this week, and once again it was pretty clear that there was a bit of a knowledge gap. Most of the crypto firms just want clear guidelines to work within - guidelines that don’t kneecap the industry.

Congress can’t decide if they think crypto is good or bad, which makes it tough to make regulation. Politico had an interesting break down of the hearing - including notes from bank lobbyists.

Bank lobbyists on the sidelines of the hearing used the opportunity to urge lawmakers to apply the same level of regulatory scrutiny to crypto startups as they do traditional lenders.

This is both good and bad - as more and more banks (and brands) foray into crypto, this could be a positive signal of recognition. But it could also result in misapplied regulation, similar to Tax Code Section 6050I.

However, the House hearing broadly went well.

Things ARE improving - but there are ways to go.

What actually is the economy?

The SEP (Summary of Economic Projections) will be released next week, which will detail how the Fed is thinking about raising rates - Goldman Sachs has laid out a very bullish case below, but it’s pretty hard to have all of that work out the way that they’ve described.

Stocks won’t be super stoked about higher rates - higher rates will put pressure on valuations and compress some growth prospects

So it’s a bit of catch-22 - you might be able to have one or the other - but probably not both.

This is also something I’ve been thinking about - what is the ceiling on the stock market? Hypothetically, as long as businesses keep growing (or memes keep memeing) the stock market should continue its trek upwards. It does go up - 53% of the time. But it’s interesting to zoom out and think - *why* exactly is it going up?

Of course if you’re bullish on the economy, bullish on certain sectors (ie clean energy, electric vehicles) the share prices of those companies should reflect those expectations of growth.

But how much growth is priced in? This is the problem with venture at the moment - it seems that companies are being priced at absurd valuations in their seed rounds - and then it’s like - well, how much higher can it actually go?

So that’s the question (truly, the infinite question that the market itself tries to answer every single day). How much growth is growth, is all growth good growth, and how much of future growth is already reflected?

Remember Voltaire - “Doubt is not a pleasant condition, but certainty is absurd”. We don’t have to know everything - but we can be strategic about the information that we have - challenge your assumptions, test your biases, and know what you don’t know. The quest for certainty is infinite, and we must constantly allow ourself open to all learning opportunities - the framework is fluid.

Disclaimer: This is not financial advice or recommendation for any investment. The Content is for informational purposes only, you should not construe any such information or other material as legal, tax, investment, financial, or other advice.